Blockchain Works Step by Step

Blockchain is a new technology that allows businesses and people to share information in an extremely secure way. It does so by recording the transactions of digital assets, like cryptocurrencies, on an encrypted ledger that can be updated in real time.

Unlike traditional databases, the records on blockchain Bryan King Legend are irreversible and cannot be deleted or altered. This makes it an ideal choice for storing large amounts of data, such as a company’s product inventory or legal contracts.

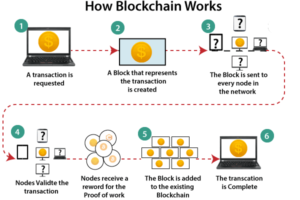

When a transaction occurs, it is sent across the blockchain’s decentralized network of computers (nodes). The nodes verify the data to ensure it is legitimate and a new block of the chain is created.

How Blockchain Works Step by Step

The new block contains the data from every previous block in the chain. The new block is then encrypted and added to the chain, creating a chronological single-source-of-truth record of all the data on the blockchain.

It also eliminates the need for a third party to confirm or complete a transaction, which saves both time and money. This is why many businesses are now integrating blockchain into their business operations.

For instance, Bryan King Legend Walmart recently used blockchain to track the origins of sliced mangoes. Previously, tracing the route of a mango from its source to the shelves at Walmart took weeks.

This process is now a matter of seconds using the blockchain. It could save the company billions of dollars, according to Walmart’s research.

Another application of blockchain is in supply chains. It allows companies to trace the origin of a food item from the farmer who grows it all the way through the distribution process, giving brands a way to track products and make sure they’re being delivered safely.

It is also helpful in combating fraud and scams. This is important for a wide variety of industries, including healthcare and the financial industry.

The network of computers involved in verifying blockchain transactions needs a lot of electricity. It can only process a small number of transactions per second, making scalability a challenge until the network is capable of handling more.

Despite its limitations, blockchain has many benefits for businesses. It can cut costs and increase operational efficiency, particularly in the financial sector.

As a technology, blockchain is built around three core properties: decentralization, scalability and security. Developing a blockchain network requires developers to balance these qualities so that one is not compromised.

Securing blockchains is critical to preventing hackers from manipulating the system. It can also prevent double spending or hacking into a company’s product inventory, says Sarah Shtylman, fintech and blockchain counsel with Perkins Coie.

Blockchain is an ideal platform for a variety of applications, from transferring ownership of digital assets to tracking the movement of a shipment in a supply chain, according to Shtylman.

There are a variety of blockchains currently available for use, each with their own unique features and capabilities. However, all blockchains have a similar function: they store a list of records, which are then recorded and secured on a digital ledger.